IN THE HIGH COURT OF MALAYA AT KUALA LUMPUR

IN THE FEDERAL TERRITORY, MALAYSIA

CIVIL SUIT NO.

BETWEEN

GLOBAL CAPITAL LIMITED

(Company No.: 2115952) … PLAINTIFF

AND

DATO’ SRI CHONG KET PEN

(NRICNo. : 540714-04-5081) … DEFENDANT

STATEMENT OF CLAIM

PARTIES

- The Plaintiff is a company incorporated in the British Virgin Islands with an address at The East Office Tower, 30thFloor, Unit 3, Jl. Lingkar Mega Kuningan Kav E3.2, No. 1, Jakarta Selatan 12950 Indonesia which through its representative(s) had invested and acquired 27.11% equity in Protasco Bhd.

- The Defendant is an individual with an address at No. 2, Jalan Bukit Seputeh, Seputeh Heights, 58100 Kuala Lumpur. The Defendant is and was at all material times a substantial shareholder of and holds executive directorship position in Protasco Bhd, a public listed company incorporated in Malaysia with its registered office at No. 802, 8thFloor, Block C, Kelana Square 17, Jalan SS7/26, 47301 Petaling Jaya, Selangor Darul Ehsan (“hereinafter referred to as Protasco”).

MATERIAL FACTS THAT LED TO THE GENESIS OF THE 3RD OF NOVEMBER 2012 AGREEMENT

- Prior to November 2012, the Defendant was a mere Director of Protasco, without any controlling or substantial interest in the latter, with only 15% equity in the same. Though being entrusted with the daily operations of Protasco, the position of the Defendant was not secured and depended heavily on the support of the then largest shareholders of Protasco, inter alia Dream Cruiser Sdn Bhd and FNQ Advanced Materials Sdn Bhd (hereinafter referred to as the 2011 Controlling Shareholders).

- Defendant was entrusted with the daily operations of Protasco due to his past experience and employment as Managing Director of Kumpulan Perunding Ikram Sdn Bhd (‘Kumpulan Ikram’), a research, development and training centre of the Malaysian Public Works Department until it’s privatisation in 1997, and now a wholly owned subsidiary of Protasco.

- However, this support began to wean, and the Defendant feared that he would be marginalised and thereafter sidelined from running the affairs of Protasco. This concern was legitimate given the following facts surrounding the financial position and reputation of Protasco under the management of the Defendant at that point of time:

a) The turnover and profits of Protasco were on a continuous decline with no visible improvement or substantial development in its core business activities, inter alia construction, engineering and trading services;

b) Further, the trading of Protasco’s shares on the stock market of Bursa Malaysia were not treated with excitement and languishing near its par value, thus reflecting the lack of interest of investors in Protasco.

- To resuscitate and revitalise Protasco, the 2011 Controlling Shareholders mooted their intention to restructure Protasco, inter alia by injecting assets and/or new businesses into the said company. This intention of the 2011 Controlling Shareholders is reflected in the following change in the management of Protasco:

a) Re designation of one Dato’ Mohd Ibrahim bin Mohd Nor from Non-Independent Director to Executive Director and Deputy Chairman of the said company on 13.6.2012;

b) Appointment of one See Ah Sing as Executive Director of the said company on 25.6.2012, replacing Defendant, and;

c) Re designation of the Defendant from the position of Executive Director to a position of a mere director in the said company on 6.2012.

- With the change in the management of Protasco, the 2011 Controlling Shareholders had the required numbers on the Board of the said company to dictate the new business direction and management of the same.

- The only option for the Defendant to elevate and strengthen his position in Protasco was to buy out the equity interest of the 2011 Controlling Shareholders in Protasco and thereafter remove those directors appointed by the latter.

RELATIONSHIP OF THE PARTIES

- This fear of losing control prompted the Defendant in securing the services of an investment banker based in Singapore, known as Andy Yong, primarily to scout for investors willing to buy-out the interest of the 2011 Controlling Shareholders in Protasco.

- Through Andy Yong, the Defendant was then introduced to the Plaintiff’s representative sometime in October 2012. A proposal was then made by the Defendant to entice the Plaintiff to invest in Protasco, inter alia by acquiring the interest of the 2011 Controlling Shareholders. However, this proposal was met with scepticism, given that the decline in the business of Protasco and business model of the latter was not within the scope of interest of the Plaintiff. To quell this lack of interest, the Defendant agreed to diversify the business of Protasco into oil and gas to enable the said company to be more attractive to the investors, provided that the Plaintiff is able to source for projects in oil and gas.

- The desperation of the Defendant to maintain control over Protasco through the Plaintiff’s acquisition of the said controlling interest became obvious. This desperation is reflected through an email correspondence between the Defendant and his son, one Kenny Chong Ther Nen (“Kenny Chong”) with the Plaintiff, whom at all material time was the Managing Director of the Property & Infrastructure Division as well as the Head of Overseas and Special Projects of Protasco.

Execution of the 3rd of November 2012 Agreement

- To give assurance that the Plaintiff’s investment in Protasco is secured, and the risk in acquiring the controlling interest from the 2011 Controlling Shareholders is insured, an agreement was executed between the Defendant and the Plaintiff on 3rd November 2012. The scheme contrived by the Defendant in this Agreement is akin to an Investment Guarantee Agreement. The Plaintiff will at trial refer to the said Agreement for its true meaning and effect.

- The recitals to the Investment Guarantee Agreement outlining the intention of the parties is reproduced as follows:-

(a) the Defendant was stated to be the beneficial owner of 41,666,667 ordinary shares in Protasco;

(b) the Plaintiff via its affiliates / nominees has been given the rights to develop and produce oil and gas in Kuala Simpang Timur, Aceh, Indonesia (“Project”);

(c) the Defendant and the Plaintiff intend to jointly develop the Project via Protasco which shall also enter into a master agreement with the Plaintiff for such a purpose; and

(d) in furtherance of the said joint development of the Project, the Defendant agreed to enter into the said Investment Guarantee Agreement in consideration for the proposed offer by the Plaintiff to acquire up to 80,429,515 ordinary shares (“Existing Protasco Shares”) representing 27.11% of the equity in Protasco from 2 parties identified as Dream Cruiser Sdn Bhd and FNQ Advanced Materials Sdn Bhd.

- In consideration for the Plaintiff acquiring the interest from the 2011 Controlling Shareholders, the Defendant agreed to as follows, vis a vis the salient terms of the Investment Guarantee Agreement:-

(a) Under Clause 1.1(a)(iv), subject to satisfactory valuation and due diligence, Protasco shall purchase 75% equity interest in the Project at a fair value to be assessed by independent professional valuer / party agreeable to the Plaintiff whose initial indicating value of the said interest being USD 55,000,000.00;

(b) Under Clause 1.1(d), after the signing of the Sale & Purchase Agreement between the Plaintiff or its nominee and the vendors in respect of the Existing Protasco Shares, the Defendant and the Plaintiff shall each nominate 1 mutually acceptable director to replace the 2 outgoing directors. Upon full settlement by the Plaintiff or its nominee of the Existing Protasco Shares, the 7 member board of directors shall have 3 members nominated by the Defendant, 3 members nominated by the Plaintiff and 1 mutually acceptable independent director;

(c) Under Clause 1.1(e), the daily operations of the existing business shall be run by the Defendant and the daily operations of the new business shall be run by the Plaintiff. The Management Executive Committee shall be equally represented by the Defendant and the Plaintiff. An Independent Advisor(s) can be engaged to help assist to resolve potential disputes. Important decisions shall be decided by the Board of Directors.

(d) Under Clause 3.1(b), for the Defendant to immediately start the process of procuring the appointment of one nominee or representative of the Plaintiff on Protasco’s Board of Directors, after the signing of the Sale and Purchase Agreement for EXISTING PROTASCO SHARES; and two nominees or representatives of the Plaintiff on Protasco ’s Board of Directors after the full settlement by the Plaintiff to the 2011 Controlling Shareholders for EXISTING PROTASCO SHARES;

(e) Under Clause 3.1(c), obtain the Plaintiff’s written agreement on any significant business decisions including, but not limited to, acquisition or disposal of significant assets, dividend payout, obtaining loans, and granting new corporate guarantees that are not mentioned in the Sale and Purchase Agreement between the Plaintiff to the 2011 Controlling Shareholders; failing which, the Defendant shall compensate in full the losses of the Plaintiff;

(f) Under Clause 3.1(f), the Defendant not to dilute the rights of the Plaintiff during the corporate exercise process;

(g) Under Clause 3.1(g), the Defendant run the existing businesses with the best endeavour and have equal rights on business decisions; and

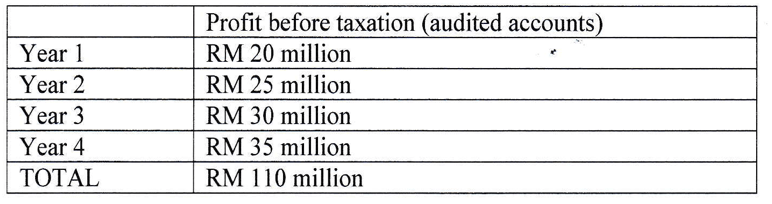

(h) Under Clause 3.1(h), the Defendant provided the following profit guarantees to the Plaintiff on existing businesses of Protasco:

with an option of early release of the guarantee when the total of RM110 million profit before taxation being met in less than 4 years.

Execution of the 26th November 2012 Share Sale Agreement

- Predicated on the guarantees given by the Defendant under the Investment Guarantee Agreement as well as the Plaintiff’s obligations therein, the Plaintiff agreed to initiate talks and negotiations with the 2011 Controlling Shareholders to acquire the latter’s interest in Protasco.

- However throughout the negotiations, the Plaintiff was represented by Messrs Manjit Singh Sachdev, Mohammad Radzi & Partners. The appointment of the said legal firm was made pursuant to the insistence and request of the Defendant, to ensure among others, the protection of the Defendant’s interest, inter alia a speedy and immediate completion of the negotiation and execution of a Share Sale Agreement to acquire the said controlling interest.

- The entire negotiations and communications with regard to the said acquisition was wholly facilitated by the Defendant as the Plaintiff were not privy to the identity of the 2011 Controlling Shareholders and/or were in contact with the same.

- The 2011 Controlling Shareholders agreed in principal to relinquish their interest in Protasco, provided that the Plaintiff agrees to acquire the Existing Protasco Shares at a huge premium of RM 1.20 per share. This proposed price is 33.33% higher than the prevailing market price for the shares trading at that point of time.

- The acquisition of the shares at a huge premium was a risk for the Plaintiff, given the performance and financial situation of Protasco. Nevertheless that risk was undertaken, given that the Plaintiff was under the impression that their investment was protected by the assurance given by the Defendant, inter alia his guarantees and obligations under the Investment Guarantee Agreement.

- To further expedite the execution of the Share Sale Agreement, the Defendant agreed to bear the cost of legal fees for the drafting and execution of the said agreement with the Plaintiff, and that the 2011 Controlling Shareholders being the vendor of the shares were excluded from bearing any legal cost in the said transaction.

- The acquisition of the 2011 Controlling Shareholders’ interest in Protasco was executed on 26.11.2012 through a Share Sale Agreement via the Plaintiff’s nominee, Kingdom Seekers Ventures Sdn. Bhd.. The interest was acquired for the price of RM 96,515,418.00, as consideration for 80,429,515 unit of shares, equivalent to 27.11% equity in Protasco .

- The salient terms of the Share Sale Agreement dated 26.11.2012 are as follows:

a) Under Clause 2.1, the Plaintiff and the 2011 Controlling Shareholders (hereinafter and specifically for this part of the statement of claim are referred to collectively as “parties”) agreed that the price for one unit of shares shall be fixed at the rate of RM 1.20;

b) Under Clause 2.1(a), the parties agreed that the Plaintiff shall acquire 58,805,373 units of shares from Dream Cruiser Sdn Bhd for RM 70,566,447.60;

c) Under Clause 2.1(b), the parties agreed that the Plaintiff shall acquire 21,624,142 units of shares from FNQ Advanced Materials Sdn Bhd for RM25,948,970.40;

d) Under Clause 2.2 (c), the directors of Protasco, who are nominees of the 2011 Controlling Shareholders are required to resign with immediate effect and relinquish their position in Protasco.

The Plaintiff will at trial refer to the said Agreement for its true meaning and effect.

- Taking into account the timing and the speed these agreements were executed, inter alia within a month, shows desperation and urgency on the part of the Defendant to ensure his control over Protasco is maintained.

- The execution of the Share Sale Agreement resulted in an immediate change in the management, financial position and the market perception of Protasco, in particular:

a) The nominee directors of the 2011 Controlling Shareholders, namely See Ah Sing, Leong Kam Wing, Dato’ Ir Syed Sis bin A. Rahman and Dato’ Mohd Ibrahim bin Mohd Noor resigned and relinquished their position in Protasco on 28.11.2012;

b) The elevation of the Defendant from the position of Director to Executive Deputy Chairman and Group Managing Director in Protasco on or about 20.2.2013;

c) The trading of Protasco’s shares started experiencing a bullish trend rising from a low of approximately RM0.90 in October 2012 (prior to the Investment GuaranteeAgreement) to more than double to approximately RM2.13 in June 2014. This had the effect of doubling the net-worth of the Defendant.

- At the outset, the execution of the Share Sale Agreement by the Plaintiff resulted in the intended effect and/or outcome envisaged in the Investment Guarantee Agreement.

Renegation of the Defendant’s Obligations under the Investment Guarantee Agreement

- While the Plaintiff had fulfilled its obligations under the Investment Guarantee Agreement, in particular the following obligations:

a) Acquiring the interest of the 2011 Controlling Shareholders, as specifically pleaded at paragraph 22above;

b) Allow and support the elevation of the Defendant from the position of Executive Director to Executive Vice Chairman and Group Managing Director in Protasco on or about 20.2.2013, as specifically pleaded at paragraph 24above;

c) Identifying for the Defendant and Protasco an oil and gas project, inter alia under the concession of PT Anglo Slavic Indonesia (“PT ASI”) via PT Haseba, in Kuala Simpang Timur, Aceh, Indonesia (“KST Oil Field”). Which Protasco had subsequently acquired interest in, via a Share Sale Agreement on 28.12.2012 (“1st Oil and Gas Agreement”) with PT Anglo Slavic Utama (“PT ASU”), the then parent company of PT ASI by making a payment of RM50 million as deposit. Further upon query by Bursa Securities Bhd on the said payment of RM50 million which is approximately 30% of the purchase consideration for the 1st Oil and Gas Agreement, the auditor of Protasco , Messrs Crowe Howarth confirmed that:

the KST oil field is genuine;

the existence of KST oil field with proven oil and gas reserve and concurs the recoverability of the deposit;

all information obtained were consistent and there were no exceptional issues raised from the audit; and

the Indonesian Central Depository’s confirmation of “Blocked Shares” to secure the said deposit were barred from trading unless otherwise instructed by the subject company and Protasco.

the Defendant had refused, failed and/or neglected to comply with his obligation under the same, (“hereinafter referred to as the act of renegation”).

- The renegation of these obligations under the Investment Guarantee Agreement by the Defendant either directly or indirectly are as particularised bellow:

Particulars of Breach

a) Contrary to Clauses 1.1(d), (e) and 3.1(b) of the Investment Guarantee Agreement, the nominee directors of the Plaintiff,Ooi Kock Aun, Tan Yee Boon, Mohamad Farid Bin Mohd Yusof and Tey Por Yee were appointed only as Non-Executive Directors of Protasco, when at that material time being the sole executive and managing director director of Protasco, the Defendant had the necessary powers to procure those appointments on the tenure as executive directors of Protasco;

b) The non-compliance in ensuring the appointments above had the effect of removing, preventing and alienating the Plaintiff from having any joint-control over the operation and business decision making process of Protasco, with respect to its ongoing businesses as well as the new business in oil and gas, as envisaged under the breached Clauses 1.1(e) and 3.1(b),(c),(g) and (f) of the Investment Guarantee Agreement;

c) Non-compliance of Clause 1.1(a)(iv) based on the following series of events:

Even without a specific valuation and due diligence on the equity of PT ASI, which the Defendant is supposed to ensure and provide under the Investment Guarantee Agreement, the independent valuers, namely RISC Operations Pty Ltd, KPMG and Grant Thornton had all came back with a valuation to support the existence of the oil and gas project in the KST Oil Field.

However despite this valuation, the Defendant had caused and/or prevented Protasco from acquiring 76% equity in PT ASI for USD 55 million, instead acquiring only 63% of the latter’s equity for USD 22 million. This had resulted in an Amended and Restated Agreement between PT ASU and Protasco on 29.1.2014 (“2nd Oil and Gas Agreement”).

The acquisition of the said equity for USD 22 million was not substantiated by the valuation reportsand was engineered solely by the Defendant to avoid the need to obtain shareholders approval of Protasco as the said acquisition would be below the 25% threshold provided for under the Bursa Malaysia Listing Requirements.

d) The Defendant failed to ensure that Protasco is profitable in particular, making a profit (before taxation) of RM30 million for Year 3 and a profit (before taxation) of RM 35 million for Year 4, as required in Clause 3.1(h) of the Investment Guarantee Agreement.

Conduct of the Defendant to consolidate power and remove the Plaintiff from having any control in Protasco

- Apart from the series of events outlined in paragraph 27above, the Defendant consolidated his control over Protasco by increasing his equity in the latter.

- This was achieved by taking advantage of the Investment Guarantee Agreement and the Share Sale Agreement which made it possible for the Defendant to acquire the balance of 38,520,150 shares in Protasco(or approximately 13% shares) from the 2011 Controlling Shareholders. This resulted in the Defendant (for the first time) being in control of 83,710,292 shares or 27.58% of Protasco. Without the investment of the Plaintiff, the Defendant would not have been able to acquire the said shares. He would be merely holding 45,190,140 shares or 15.23% of the said company.

- Upon consolidating his power and control over the management and operation of Protasco, with him as the sole Executive and Managing Director with substantial controlling interest in the said company, the Defendant set into motion and/or caused the following series of events intended either directly or indirectly to remove any influence and/or control the Plaintiff has either directly or through its representatives in Protasco:

a) The frustration and/or wrongful termination of the 2nd Oil and Gas Agreement between Protasco and PT ASU on 4.8.2014, while at that material time having control of PT ASI via Protasco;

b) The false accusation and false police report, against the nominee directors of the Plaintiff, namely, Ooi Kock Aun and Tey Por Yee, inter alia for allegedly making a false declaration to Bursa Malaysia that they have no interest and/or are not shareholders and directors of PT ASU. A false accusation that caused the arrest, freezing, seizure of assets and shares, and charging of those nominee directors under the Penal Code, whom were later discharged upon withdrawal of the charges by the Public Prosecutor;

c) Forming of a purported investigation committee to investigate the oil and gas agreements based on the allegations under paragraph 30(b) above;

d) Causing and engineering the removal of the said nominee directors of the Plaintiff via an Extraordinary General Meeting (EGM) on 26.11.2014, based on the allegations under paragraph 30(b) above;

e) Causing a suit against the said nominee directors of the Plaintiff and PT ASU for fraud and breach of the oil and gas agreements via suit No. 22NCC-362-09/2014.

- Apart from removing the Plaintiff and/or its nominees from Protasco, it also served the purpose of deflecting the attention and scrutiny of Bursa Malaysia and Securities Commission Malaysia on the management of Protasco under the stewardship of the Defendant.

- With the removal of the Plaintiff from having any control and/or influence in Protasco, the Defendant proceeded to use his position and control in the said company to dictate and enter into business transactions and decisions on matters of operation, remuneration, payments of dividends and salaries for his own benefit and enrichment while at the expense and best interest of the said company. The Plaintiff will at trial refer to the relevant Annual Reports of Protasco to support this claim.

Damages and losses suffered by the Plaintiff

- As a consequence of the breaches by the Defendant as pleaded at paragraphs 27(a), (b), (c) and (d) above, and the misconduct by the Defendant through Protasco as pleaded at paragraphs 30(a), (b), (c), (d) and (e), the Plaintiff has suffered irreparable loss and damage to their investment, reputation, credibility and business.

- The full particulars of the losses and damages suffered by the Plaintiff will be disclosed at the trial of this suit, and brief particulars are set out hereunder as follows:

Particulars

a) Loss of investmentand future profits for acquiring80,429,515 unit of shares, equivalent to 27.11% equity in Protasco;

b) Loss of margin to finance the acquisition of shares up to RM75million;

c) Liability of USD 55 million to PT ASU, as guarantor for the Defendant pursuantto the Investment Guarantee Agreement;

d) Legal fees incurred by the Plaintiff through its representatives in relation to matters pleaded under paragraph 30(b) above.

35. Thus the losses and damages above have been incurred either directly and/or indirectlyas a result of the said breaches and misconduct of the Defendantwhich the Plaintiff will claim as general damages.

36. Therefore the Plaintiff further claims for the following reliefs:

a) A declaration that the Defendant has acted in breach of the Investment Guarantee Agreement;

b) A sum of RM 65,000,000.00 as payment for the Profit Guarantee under Clause 3.1(h) of the Investment Guarantee Agreement;;

c) A declaration that the Defendant is liablefor USD 55,000,000.00, a figure that the Plaintiff has guaranteed to PT ASU as a result of the Defendant’s obligation under Clause 1.1(a)(iv) of the Investment Guarantee Agreement;

d) An account and inquiry of all the gains and profits made by the Defendant pursuant to the Investment Guarantee Agreement;

e) Aggravated and / or exemplary damages, to be assessed against the Defendant in respect of the breaches of the Investment Guarantee Agreement; and

f) General Damages;

g) Costs; and

h) Any further and/or reliefs or order as this Honourable Court deems just and proper.